Farm Loans in USA 2026 – Things Farmers Should Check Before Borrowing

Best Farm Loans in USA , farming in the USA is not getting cheaper. Anyone who has tried to buy land, repair a tractor, hire help, or even stock up on feed already knows that. The numbers can get uncomfortable fast.

For a new farmer, the biggest problem is usually getting started. For an existing farmer, the problem may be different. Maybe the equipment is getting old. Maybe rented land is becoming harder to keep. Maybe cash is tight before harvest. These are the kinds of situations where farm loans become part of the conversation.

A farm loan is simply money borrowed for agricultural use. It may be used to buy land, purchase equipment, pay seasonal expenses, add livestock, build fencing, repair barns, or keep the farm running during a slow cash-flow period.

But taking a farm loan should not be treated like a quick fix. A loan can help a farm grow, but it can also create pressure if the payment schedule does not match the farm’s income cycle.

What Are Farm Loans Used For?

Farm loans are usually connected to real farm needs. Some farmers borrow because they want to buy acreage. Others need a tractor, irrigation setup, livestock trailer, storage building, or working capital for the season.

Common uses include:

- buying farmland

- paying for seed, feed, fertilizer, or fuel

- purchasing livestock

- repairing or replacing equipment

- building fences, barns, or storage

- covering labor and operating costs

- expanding an existing farm

- recovering after crop or property damage

A vegetable grower, cattle rancher, dairy farmer, poultry operator, or grain producer may all need financing, but not for the same reason. That is why choosing the right loan matters.

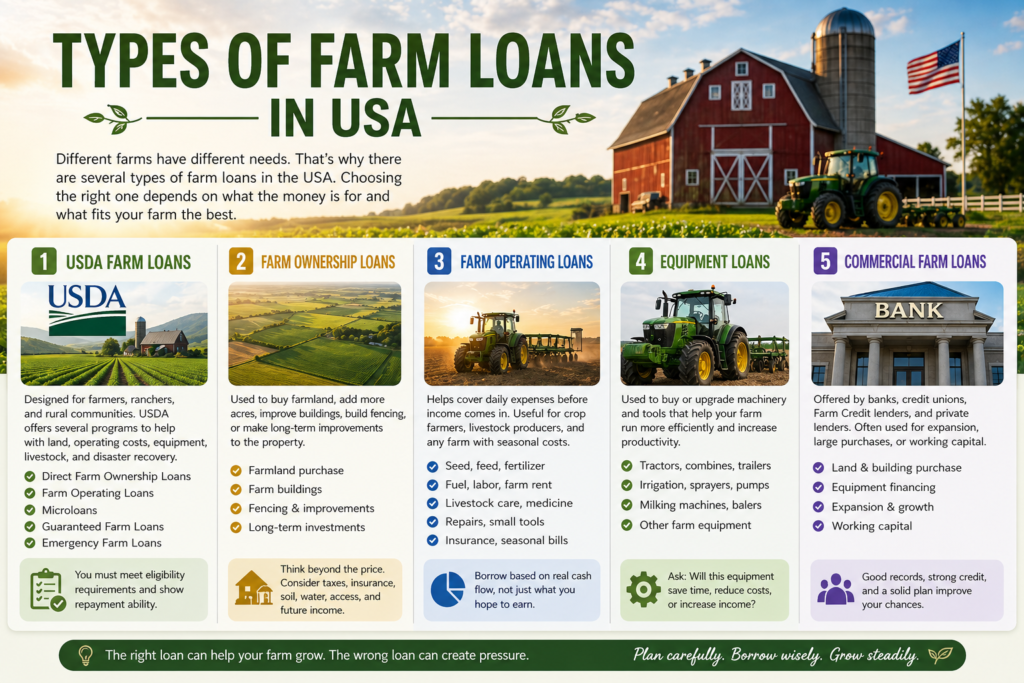

Types of Farm Loans in USA

Farm loans can be confusing at first. People often search for one simple loan, but farming does not really work that way. A person buying 40 acres of land has a different need than someone trying to pay for seed, feed, fuel, or a tractor repair before the season starts.

That is why lenders usually ask what the money is for. They want to know if the loan is for land, daily farm expenses, equipment, livestock, repairs, or expansion. Once that part is clear, choosing the right loan becomes easier.

Here are the main farm loan types farmers in the USA usually look at.

1. USDA Farm Loans

USDA farm loans are common among new farmers, small farm owners, ranchers, and family farms. Many people check these first because the programs are made for agriculture, not regular personal borrowing.

There are different USDA loan programs. Some help with land. Some help with operating costs. Some are smaller loans for new or smaller farms. Others are connected to disaster recovery.

Common USDA farm loan options include:

- Direct Farm Ownership Loans

- Farm Operating Loans

- Microloans

- Guaranteed Farm Loans

- Emergency Farm Loans

A USDA farm loan may help a farmer buy land, purchase livestock, repair buildings, buy equipment, or cover farm operating costs. But the use depends on the exact program.

One thing should be clear. USDA loans are helpful, but they are not automatic. A farmer still has to meet eligibility rules, show repayment ability, and provide documents. If the numbers are not clear, approval can become harder.

For a beginner, this can still be a good place to start. A simple plan, honest income estimate, and basic farm records can help a lot.

2. Farm Ownership Loans

Farm ownership loans are mostly for land and farm property.

A farmer may use this type of loan to buy farmland, add more acres, improve buildings, build fencing, or make long-term improvements to the property.

For many farmers, owning land is a big goal. Renting land can work for a while, but it does not always feel secure. If the lease ends or the rent goes up, the whole farm plan can change. Owning land gives more control, but it also brings more responsibility.

Before taking a farm ownership loan, the land price is not the only thing to check. You also need to think about taxes, insurance, drainage, soil quality, road access, water access, repairs, and whether the land can actually produce enough income.

That is why farm ownership loans are often linked with farm land loans. They are not just for buying property. They are usually part of a long-term farm plan.

3. Farm Operating Loans

Farm operating loans are for the everyday costs of running a farm.

This is the kind of loan many farmers need before they earn money from the season. A crop farmer may spend a lot on seed, fertilizer, fuel, and labor before harvest. A cattle farmer may need feed, medicine, fencing, or pasture costs before selling animals.

Operating loans may be used for:

- seed

- feed

- fertilizer

- fuel

- labor

- farm rent

- livestock care

- equipment repairs

- small tools

- insurance

- seasonal bills

This loan can be useful because farm expenses do not wait until income arrives. Bills may come early, while sales may come months later.

Still, operating loans need careful planning. If crop prices fall, animals sell later than expected, or weather causes delays, repayment can become stressful. So the loan amount should match the farm’s real cash flow, not just the amount the farmer hopes to borrow.

4. Equipment Loans

Equipment loans are used for farm machinery.

This may include tractors, combines, irrigation systems, trailers, balers, sprayers, milking machines, pumps, and other tools needed for daily work.

Farm equipment is expensive. Even used equipment can cost a lot. Many farmers cannot pay the full amount at once, so they finance it over time.

An equipment loan can make sense when the machine helps the farm save time, reduce repair costs, or increase production. But it should not be taken only because new equipment looks attractive.

Before borrowing, it is worth asking:

- Will this machine actually help the farm earn or save money?

- Can the farm make the payments during slow months?

- Is a used machine enough for now?

- How much will repairs and maintenance cost?

- How long will the equipment last?

In many equipment loans, the machinery itself may be used as collateral. That can help with approval, but it also means missed payments can put the equipment at risk.

5. Commercial Farm Loans

Commercial farm loans are offered by banks, credit unions, Farm Credit lenders, and private agricultural lenders.

These loans can be useful for farmers who need larger amounts or more flexible terms. Established farms often use commercial loans for expansion, equipment, land, buildings, or working capital.

The requirements are usually stricter. A lender may check credit score, tax returns, bank statements, farm income, debt, collateral, and repayment history.

For a brand new farmer, commercial loans may be harder to get. For an established farmer with good records, they may be a strong option.

One thing to remember is that not every bank understands farming. Farm income may not come every month like a regular paycheck. Some farms earn most of their money after harvest or after livestock sales. A lender who understands agriculture may be easier to work with than a lender who only looks at monthly income.

How to Pick the Right Farm Loan ?

The right loan depends on the reason you need money.

If you want to buy land, farm ownership loans or farm land loans may be the right direction. If you need money for seed, feed, fertilizer, fuel, or labor, an operating loan may fit better. If the main issue is machinery, then an equipment loan may make more sense. If you are a new farmer or running a small operation, USDA farm loans or microloans may be worth checking.

Do not choose a loan only because the lender offers a big amount. Bigger is not always better. A loan should match the farm’s income and repayment ability.

Before applying, write down the real purpose of the loan. Then write down the expected cost and when the farm will have money to repay it. This simple step can prevent a lot of stress later.

A farm loan should make the farm stronger. It should not make every season feel heavier.

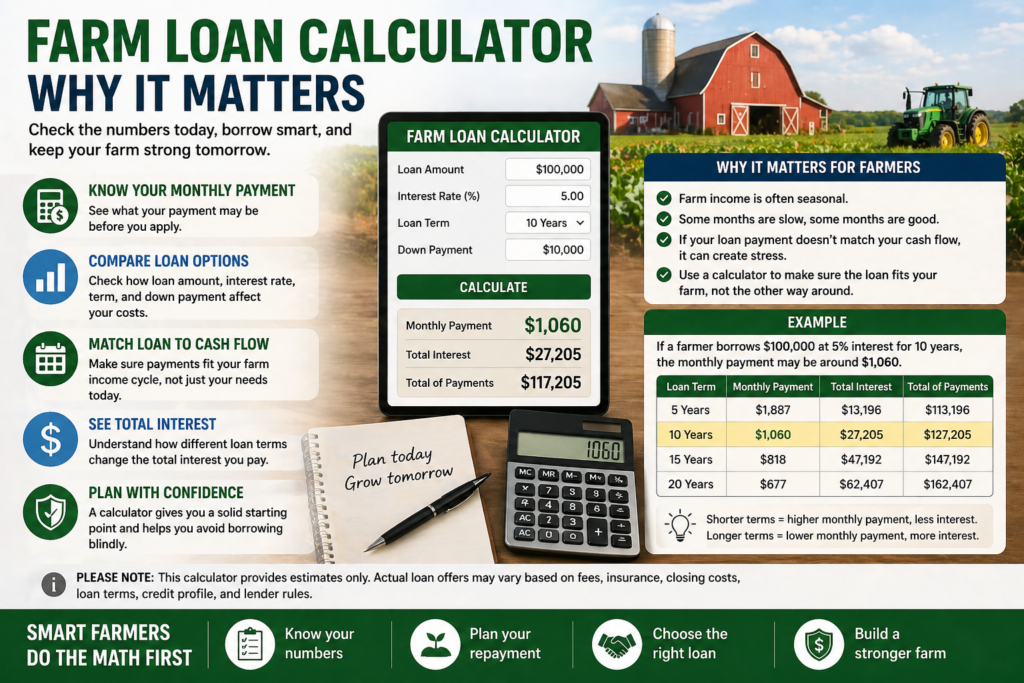

Farm Loan Calculator – Why It Matters

Before applying for a farm loan, it is better to check the numbers first. Many farmers only think about how much money they need, but the monthly payment is just as important.

A farm loan calculator helps you get a rough idea of what the loan may cost. It can show the monthly payment, total interest, and how different loan terms affect your budget.

This is useful because farm income is not always the same every month. Some farms earn most of their money after harvest. Some depend on livestock sales. Others may have seasonal income from markets, contracts, or wholesale buyers. If the loan payment does not match the farm’s cash flow, even a useful loan can become stressful.

A farm loan calculator or farm credit loan calculator can help you compare things like loan amount, interest rate, repayment term, and down payment. It also helps you see whether a shorter loan term is too expensive or whether a longer term will cost too much in interest over time.

For example, if a farmer borrows $100,000 at 5% interest for 10 years, the monthly payment may be around $1,060. That number may look manageable for one farm, but too high for another. This is why checking the payment before applying is important.

A calculator will not give the final lender offer. The actual payment can change because of fees, loan terms, insurance, closing costs, or lender rules. Still, it gives you a starting point and helps you avoid borrowing blindly.

Interest Rates for Farm Loans in 2026

Farm loan interest rates in 2026 can be different from one lender to another. There is no single rate that applies to every farmer.

A USDA-backed loan may have a lower rate than a private lender. A bank loan may fall somewhere in the middle, depending on the borrower’s credit and farm records. Private lenders may approve faster in some cases, but their rates can be higher.

As a rough idea, farmers may see rates like:

- USDA loans: around 3% to 6%

- Bank loans: around 5% to 9%

- Private lenders: around 7% to 12%

These numbers are only general estimates. The actual rate depends on the lender, market conditions, loan type, and the borrower’s profile.

A farmer with good credit, steady farm income, strong records, and valuable collateral may qualify for better terms. A new farmer with limited records or weak credit may face a higher rate or stricter requirements.

Lenders usually look at things like credit score, farming experience, loan amount, collateral, debt, income, and repayment ability. They may also check whether the farm has a clear plan for using the money.

Before choosing a loan, do not look only at the interest rate. Also check the repayment schedule, fees, down payment, prepayment rules, collateral requirements, and total loan cost.

A slightly lower rate is helpful, but the loan still needs to fit the farm’s real income cycle. The best farm loan is not always the biggest one or the fastest one. It is the one your farm can repay without putting too much pressure on the business.

How to Get Approved Faster for Farm Loans in USA

Getting a farm loan approved quickly is not only about filling out an application. Most delays happen because the farmer does not have the right documents ready, the numbers are unclear, or the loan purpose is not explained properly.

A lender wants to know three basic things: why you need the money, how the farm will use it, and how you plan to repay it. If you can answer these clearly, the process usually becomes smoother.

Prepare a Simple but Clear Business Plan

A farm business plan does not need to sound complicated. It just needs to show that you understand your farm and your numbers.

Lenders may want to see what you grow or raise, how much income you expect, what your main expenses are, and what risks could affect the farm. For a crop farm, this may include planting plans, expected yield, market price, buyers, and seasonal costs. For a livestock farm, it may include herd size, feed costs, veterinary expenses, selling timeline, and expected revenue.

A good plan should explain:

- what the loan will be used for

- how the farm makes money

- expected income and expenses

- crop or livestock plans

- possible risks

- repayment plan

Do not overstate the numbers just to impress a lender. Realistic numbers are better than big promises.

Work on Your Credit Before Applying

Credit score matters in many farm loan applications, especially with banks and private lenders. A stronger credit profile can help you qualify for better terms.

Some lenders may prefer borrowers with scores around 680 or higher, but this is not a fixed rule for every loan. USDA programs, credit unions, and agricultural lenders may look at the full picture, not just the score.

Before applying, check your credit report if possible. Pay down small debts, avoid late payments, and do not apply for too many loans at the same time. Even small improvements can help.

Show Farming Experience

Farming experience can make lenders more comfortable. It shows that you understand the work, the costs, and the risks.

Experience does not always mean owning a large farm for many years. Small-scale farming, working on a family farm, managing livestock, growing produce for local markets, or helping with farm operations can also matter.

If you are a beginner, be honest about it. Explain what experience you do have and where you are getting advice or support. A new farmer with a clear plan may look better than an experienced farmer with poor records.

Offer Collateral When Needed

Collateral gives the lender extra security. It may include land, equipment, livestock, vehicles, or other farm assets.

Not every loan requires the same collateral, but having assets available can improve approval chances. It may also help with larger loan amounts.

Still, farmers should be careful. If you use land or equipment as collateral, missed payments can put those assets at risk. Do not offer more than you understand.

Check USDA Farm Loan Programs

USDA farm loans are worth checking, especially for beginning farmers, smaller farms, and borrowers who may not qualify easily through regular banks.

USDA options may include farm ownership loans, operating loans, microloans, guaranteed loans, and emergency loans. Each program has different rules, so it is important to match the loan with the purpose.

For example, a microloan may work for a smaller operation, while a farm ownership loan may fit someone buying land. An operating loan may be better for seed, feed, fuel, labor, or seasonal expenses.

USDA loans can be helpful, but they still require paperwork. Having records ready before applying can save time.

Choose the Right Lender

Not every lender understands farming. This matters because farm income is often seasonal. A regular lender may expect monthly income like a normal paycheck, while a farm lender may understand that income often comes after harvest or livestock sales.

Farmers can compare:

- local banks

- credit unions

- Farm Credit institutions

- USDA Farm Service Agency

- private agricultural lenders

- equipment financing companies

Do not choose a lender only because they say “fast approval.” Check the rate, fees, repayment schedule, collateral rules, and total cost of the loan.

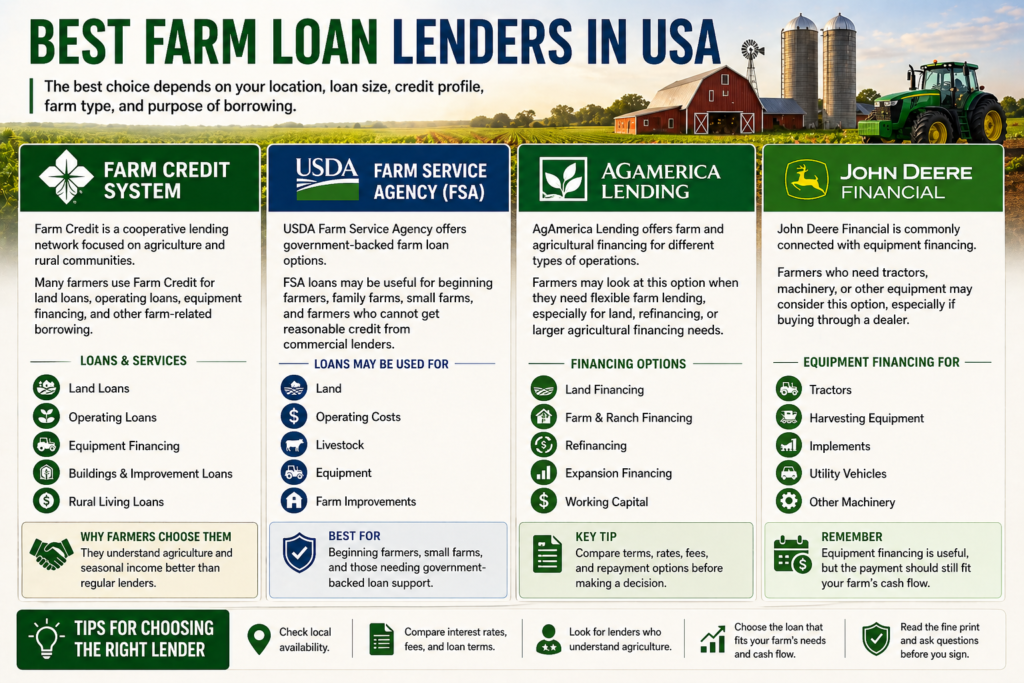

Best Farm Loan Lenders in USA

There are several lenders and institutions farmers often consider. The best choice depends on your location, loan size, credit profile, farm type, and purpose of borrowing.

Farm Credit System

Farm Credit is a cooperative lending network focused on agriculture and rural communities. Many farmers use Farm Credit for land loans, operating loans, equipment financing, and other farm-related borrowing.

Because they work closely with agriculture, they may understand seasonal income better than regular lenders.

USDA Farm Service Agency

USDA Farm Service Agency is one of the most important places to check for government-backed farm loan options.

FSA loans may be useful for beginning farmers, family farms, small farms, and farmers who cannot get reasonable credit from commercial lenders. These loans may help with land, operating costs, livestock, equipment, and farm improvements.

AgAmerica Lending

AgAmerica Lending offers farm and agricultural financing for different types of operations. Farmers may look at this option when they need flexible farm lending, especially for land, refinancing, or larger agricultural financing needs.

As with any private lender, compare terms carefully before applying.

John Deere Financial

John Deere Financial is commonly connected with equipment financing. Farmers who need tractors, machinery, or other equipment may consider this option, especially if they are buying through a dealer.

Equipment financing can be useful, but the payment should still fit the farm’s cash flow.

Benefits of Farm Loans

A farm loan can help when it is used for the right reason. It can give a farmer access to capital without waiting years to save the full amount.

Farm loans may help with land purchases, equipment upgrades, operating expenses, livestock, building improvements, and business expansion. They can also help farmers manage seasonal cash flow.

The benefit depends on how the money is used. A loan that improves production or solves a real cash flow problem may support growth. A loan taken without a plan can create stress.

Common Mistakes to Avoid

One common mistake is applying without a clear plan. Lenders need to know exactly where the money will go.

Another mistake is borrowing more than the farm can handle. A large loan may look helpful at first, but the payments can become heavy during slow months.

Farmers should also avoid ignoring the fine print. Interest rate matters, but so do fees, repayment dates, collateral requirements, late payment rules, and prepayment terms.

It is also risky to accept the first offer without comparing lenders. Two lenders may offer very different terms for the same loan amount.

Practical Tips Before Borrowing

Before borrowing, calculate whether the loan can actually improve the farm. If you are buying equipment, ask whether it will save labor, reduce repair costs, or increase production. If you are buying land, check whether the land can generate enough income to support the payment.

Keep farm records organized. Track sales, expenses, repairs, feed costs, seed costs, fuel, labor, rent, and loan payments. Good records help with both approval and long-term farm management.

Use a farm loan calculator or farm credit loan calculator before applying. It can help you estimate payments and compare loan terms.

It also helps to build a relationship with lenders before you urgently need money. A lender who already understands your farm may be easier to work with later.

Summary Table: Farm Loan Types in the USA

| Farm Loan Type | Best For | Common Uses | Main Thing to Check Before Borrowing |

|---|---|---|---|

| USDA/FSA Farm Loans | Beginning farmers, family farms, small farms, and farmers who may not qualify easily through regular lenders | Land, livestock, equipment, farm buildings, operating costs, and farm improvements | Check eligibility, repayment ability, paperwork requirements, and current FSA rates. |

| Farm Ownership Loans | Buying, enlarging, or improving farmland | Buying land, closing costs, farm buildings, conservation improvements, and land expansion | Check land productivity, taxes, insurance, drainage, water access, and long-term repayment. |

| Farm Operating Loans | Seasonal and day-to-day farm costs | Seed, feed, fertilizer, fuel, livestock, equipment, labor, family living costs, and farm operating expenses | Match repayment dates with harvest, livestock sales, or seasonal income. |

| Microloans | Small farms, beginning farmers, specialty farms, and non-traditional operations | Smaller ownership or operating needs | Check whether the $50,000 cap is enough for your farm needs. |

| Equipment Loans | Machinery and tools | Tractors, combines, trailers, irrigation systems, pumps, balers, sprayers, and other equipment | Ask whether the equipment will increase income, reduce labor, or lower repair costs enough to justify payments. |

| Commercial Farm Loans | Established farms needing larger or flexible financing | Land, expansion, refinancing, working capital, buildings, and equipment | Compare rate, fees, collateral, term, lender experience with agriculture, and cash-flow fit. |

| Emergency Farm Loans | Recovery after qualifying disasters or losses | Production losses, physical losses, and disaster recovery | Confirm disaster eligibility, actual-loss amount, documentation, and repayment terms. |

2026 Farm Loan Rate Snapshot

| Loan / Rate Item | April 2026 Rate or Rule | Notes |

|---|---|---|

| FSA Direct Farm Operating Loan | 4.750% | Effective April 1, 2026. |

| FSA Operating Microloan | 4.750% | Same posted rate as Direct Operating. |

| FSA Direct Farm Ownership Loan | 5.750% | Effective April 1, 2026. |

| FSA Farm Ownership Microloan | 5.750% | Same posted rate as Direct Farm Ownership. |

| FSA Direct Farm Ownership — Joint Financing | 3.750% | Effective April 1, 2026. |

| FSA Farm Ownership — Down Payment | 1.750% | Effective April 1, 2026. |

| FSA Emergency Loan — Amount of Actual Loss | 3.750% | Effective April 1, 2026. |

| Guaranteed Farm Loans | Lender-set, subject to USDA maximums | Guaranteed loan rates depend on the lender and USDA maximum-rate rules. |

Farmer Checklist Before Borrowing

| What to Check | Why It Matters |

|---|---|

| Loan Purpose | A land loan, operating loan, equipment loan, and emergency loan solve different problems. Choosing the wrong loan can create repayment pressure. |

| Real Repayment Ability | Farm income is often seasonal, so payments should match harvest income, livestock sales, contract payments, or market cash flow. |

| Total Cost, Not Just Rate | Fees, closing costs, insurance, down payment, collateral, late fees, and prepayment rules can change the real cost. |

| Collateral Risk | Land, livestock, machinery, or other assets may be at risk if payments are missed. |

| Farm Records | Lenders usually want clear income, expenses, tax records, production history, debt, and a repayment plan. |

| Credit Profile | Stronger credit may improve approval chances and loan terms, especially with banks and private lenders. |

| Lender Fit | A lender familiar with agriculture may better understand seasonal income than a general consumer lender. |

| Loan Calculator Result | A calculator helps estimate monthly payment, total interest, and whether the loan fits the farm’s budget before applying. |

| USDA/FSA Options | USDA/FSA loans may be useful for beginning farmers, family farms, and borrowers who cannot get reasonable commercial credit. |

| Backup Plan | Weather, price drops, delayed sales, animal health issues, or equipment failure can affect repayment. |

Final Thoughts

Farm loans in the USA can help farmers buy land, cover operating costs, purchase equipment, add livestock, or expand their business. But fast approval usually comes from preparation, not luck.

Before applying, know why you need the money, how much you really need, and how the farm will repay it. Compare lenders, check the full loan terms, and use a farm loan calculator before making a decision.

The right loan can support growth. The wrong loan can make every season harder. So apply carefully, keep your records clean, and choose financing that fits the farm’s real income cycle.

References

- USDA Farm Service Agency — Farm Loan Programs: Explains FSA farm loan options and their role in helping farmers start, expand, or maintain a family farm.

- USDA Farm Service Agency — Current FSA Loan Interest Rates: Provides April 2026 FSA loan rates and guaranteed-loan maximum-rate rules.

- USDA FSA News Release — April 2026 Lending Rates: Confirms April 1, 2026 effective rates for operating, ownership, emergency, commodity, and storage facility loans.

- USDA Farm Service Agency — Farm Ownership Loans: Details Farm Ownership Loan uses, limits, down payment loan rules, and repayment terms.

- USDA Farm Service Agency — Microloan Programs: Explains microloan limits, simplified requirements, and repayment terms.

- Farm Credit — About/Structure: Describes Farm Credit as a nationwide customer-owned cooperative network serving farmers, ranchers, agribusinesses, and rural communities.

- John Deere Financial — Farm Equipment Loans & Leases: Covers equipment financing and leasing options for farm machinery.

FAQs for best Farm Loans in USA

1. What is the easiest farm loan to get?

For someone new to farming, a smaller loan is often the easiest place to start. Many farmers look at USDA microloans because they are made for smaller farm needs, not big purchases.

Of course, the lender will still check a few things. They may look at your income, farm plan, repayment ability, and whether your papers are complete.

2. How long does farm loan approval take?

There is no fixed timeline. Some applications move faster when everything is ready from the start. In many cases, it can still take a few weeks.

The process may slow down if income records, land details, collateral papers, or other documents are missing.

3. Can I get a farm loan with poor credit?

It may be possible, but it can be harder. A lender may want to see something that lowers their risk, such as collateral, steady income, or a clear repayment plan.

A co-signer can also help in some cases. Some government-backed programs may consider more than credit score, but repayment ability matters most.

4. What can I use a farm loan for?

Farm loans can cover many farming costs. This may include land, equipment, livestock, seeds, feed, fertilizer, fuel, repairs, fencing, labor, buildings, or daily farm expenses.

Some loans may also be used to grow or improve an existing farm.

5. Are USDA loans better than bank loans?

It depends on the farmer. USDA loans may be useful for beginners or farmers who have trouble qualifying at a bank.

Bank loans may be better for farmers with strong credit, stable income, and good records. The right option depends on your situation.

Thesis Link : https://saulibrary.edu.bd/daatj/public/uploads/BAU200601_19-Pp_5.pdf

- White Spots on Zucchini Leaves Not Powdery Mildew? 5 Causes - July 29, 2026

- Remote Control Lawn Mower Buyer’s Guide -4 Critical Features - July 27, 2026

- Why Fruit Trees Die Suddenly – Common Diseases Guide - June 26, 2026